Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If we let the media determine the mood regarding the housing market, it would be time to shut the party down and call it a night. I’m here to report that we are still dancing and there is a lot to celebrate! While it is not all shiny and bright (it never is), there is a pattern of consistent growth and the sky is far from falling. The environment has changed from a year ago and we are still moving to the beat of the drum despite some rain (insert dancing emoji here).

The latest headline from the Seattle Times claims that prices have tumbled from last year. While prices are down from a year ago the story is much more detailed and it is far from a tumble. The DJ (The Fed) played some songs (hiked rates) that cleared the dancefloor for a bit, but the hits are playing now and demand is strong! The headline I have included above is a much more accurate depiction of the pricing journey over the last year and a half, and it is actually pretty great.

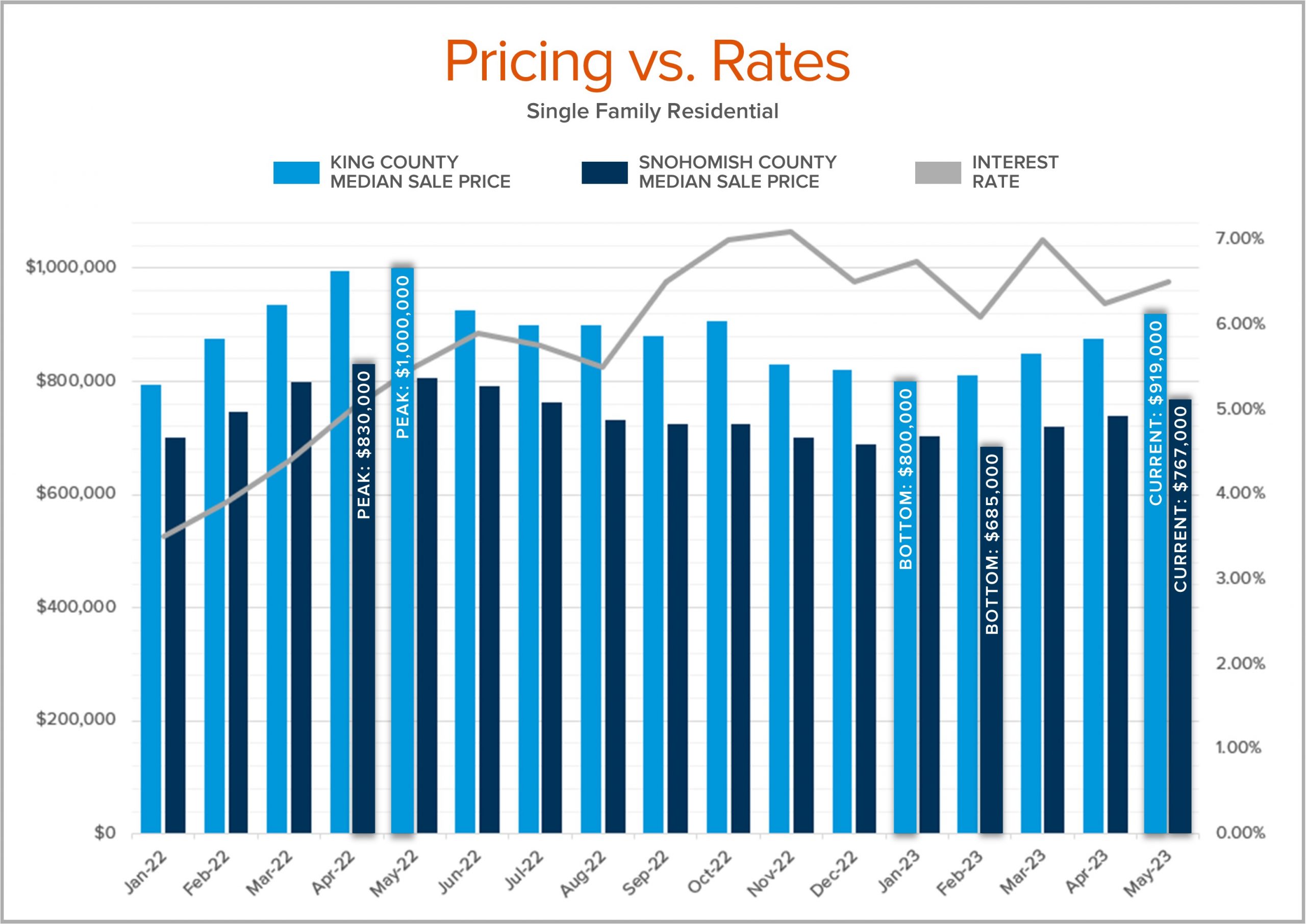

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In Snohomish County, the median price peaked in April 2022 at $830,000 and is currently at $767,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in February 2023 at $685,000 which was down 17% (the actual tumble) from the peak but are now up 12% from the bottom!

This was a relatively quick correction that is trending in a positive direction as the market gets used to higher interest rates. Quantitative Easing could not last forever and rates had to go up to combat inflation. During the same time frame detailed above, interest rates dramatically changed.

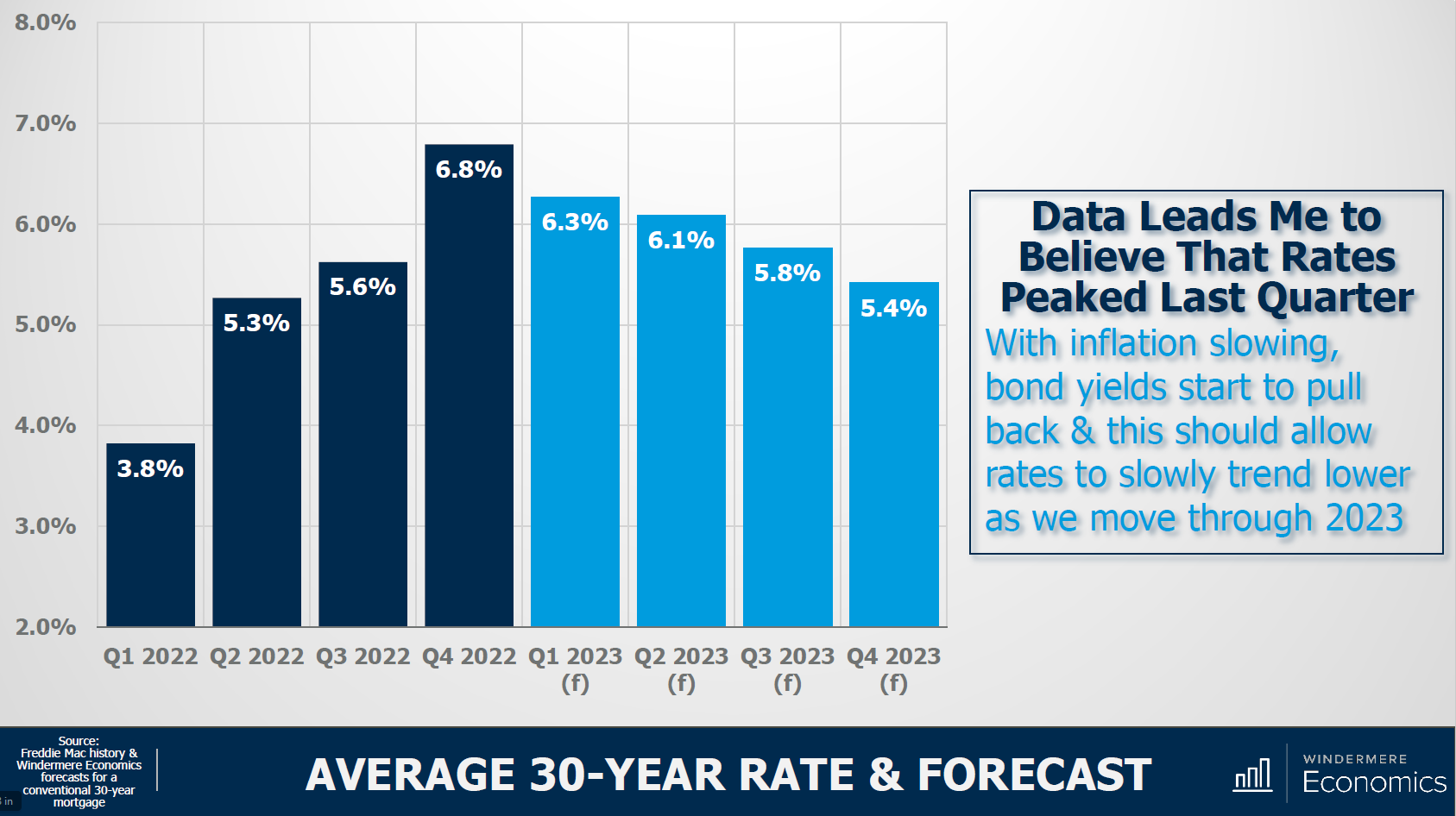

In May 2022, they averaged 5.5% (the peak) and in January 2023 they averaged 6.75% (the bottom). In fact, they started 2022 at 3.5%, a level we will likely never see again! Currently, rates are hovering in the high 6% and are predicted to slowly recede as we enter the second half of 2023. Proof that buyers have become conditioned to the new normal of rates is that prices have grown from the start of 2023 (January – May 2023): 14% in King County and 11% in Snohomish County, despite rates remaining in the 6% and at times cresting 7%. When they go down to the lower 6% or even the high 5%, expect prices to climb at a faster rate. Will there be a buyer mosh pit? Buyers should be weighing these effects as they choose when to act. Rates can always be re-financed, but the sale price cannot.

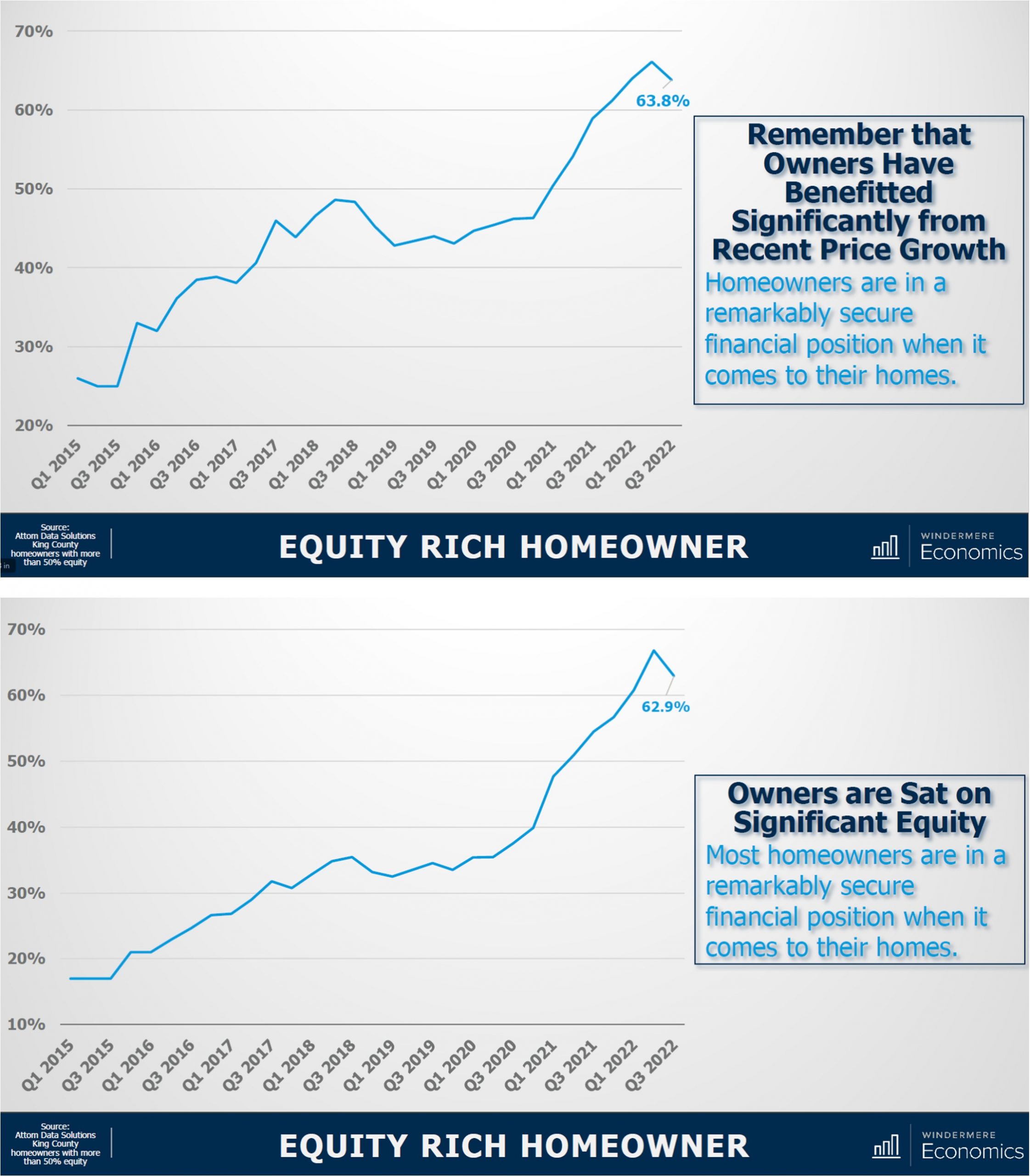

While the homeowners that purchased during those peak months have some time before they regain their home’s value, it will happen. We are a year out from the peak and the last time we had a correction in 2018 it took 17 months to recover. That subsection of sales aside and equity levels are strong. Imagine the hope you feel when watching the first dance at a wedding to the classic It’s A Wonderful World; the party is just getting started. Prices are up in King County by 27% from March 2019 to March 2023 and in Snohomish County up 46%. Ten-year gains are astounding at 140% in King County and 179 % in Snohomish County.

This leads me to my biggest takeaway; real estate moves are dictated by life changes. Maybe the DJ plays Sweet Home Alabama and you rush to the dance floor because it’s time to move closer to family, or Marry You inspires you to take the plunge into married life as you spin the night towards household formation. My point is, change drives demand.

While real estate is an investment, it is also where we live. It is our refuge, our security, and our joy. We usher in pleasure and pain in the four walls we call home and at some point, that will lead to wanting something more, less, or just different out of our home. I understand that these moves may have been put on hold while the DJ figured out the crowd. Currently, the dance floor is becoming more crowded. The attendees at the party are realizing that we only live once and that we are not going back to the discotheque of 3-4% interest rates; they are ready to boogie!

The dancing/party metaphor was a fun way to tell a complicated and emotional story. This correction and recovery have been a bit hard and confusing, especially after the disruption of the pandemic. We are just getting our dancing shoes broken in again. If life has met you at a crossroads of change and you are curious about how real estate relates to this for you, please reach out. I am deeply invested in the data and my service is always rooted in educating my clients. It is my goal to help the people I serve navigate smooth transitions that are financially stable and strong and match their homes to their hearts.

Windermere Community Service Day

Windermere Community Service Day

Since 1984, Windermere associates have dedicated a day of work to complete neighborhood improvement projects as part of Windermere’s Community Service Day. After all, real estate is rooted in our communities. And an investment in our neighborhoods gives us all a better place to call home.

This Friday, my office will spend the day with the Snohomish Garden Club working to put fresh produce on the tables of local families who need a little help. We will plant over a half-acre of veggies and fruits that will be harvested over the summer and into the fall.

If you’d like to pitch in, you can donate to our Summer Food Drive, or bring donations to my office, through August 4th. All donations will go to Volunteers of America Western WA food banks.

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

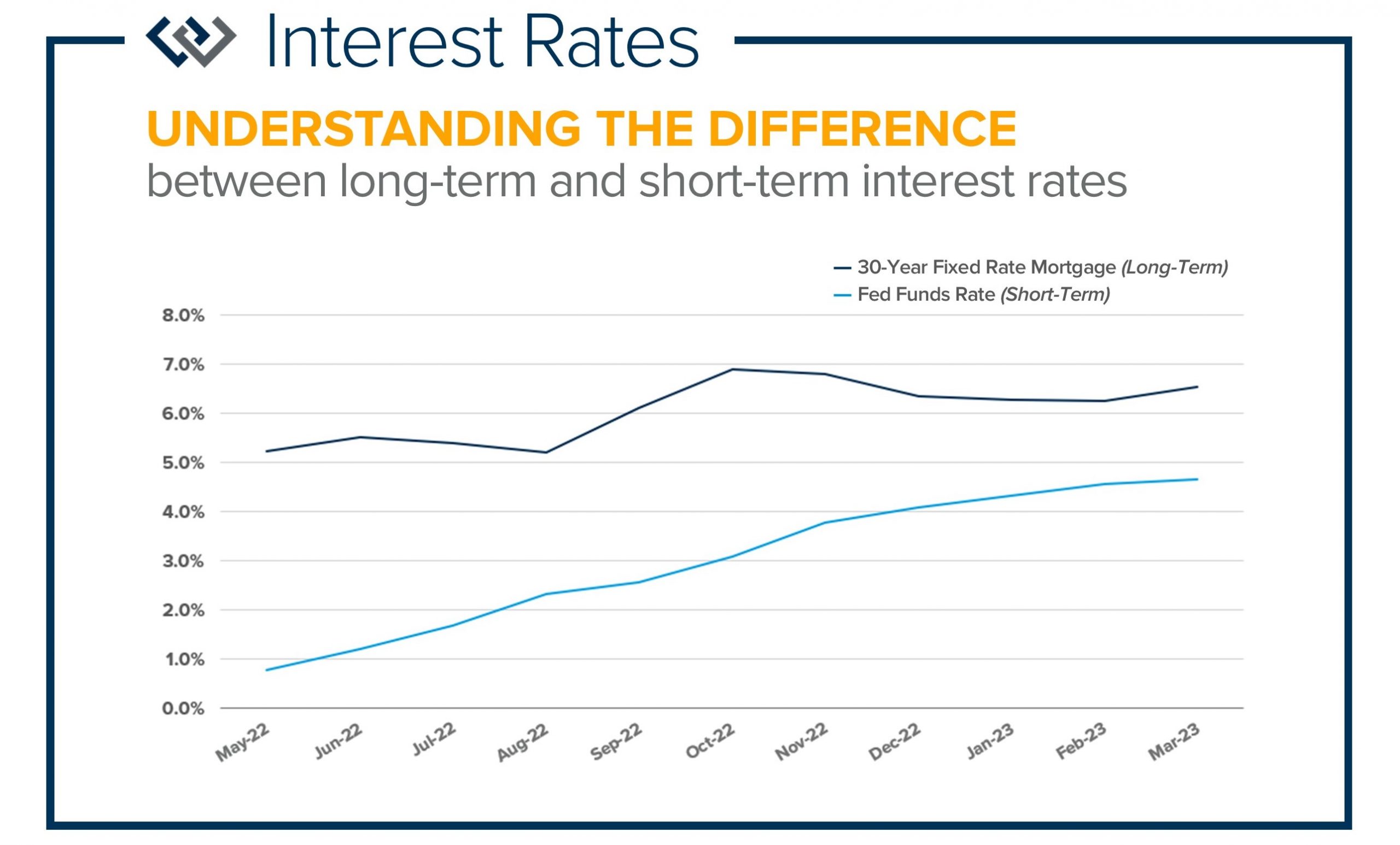

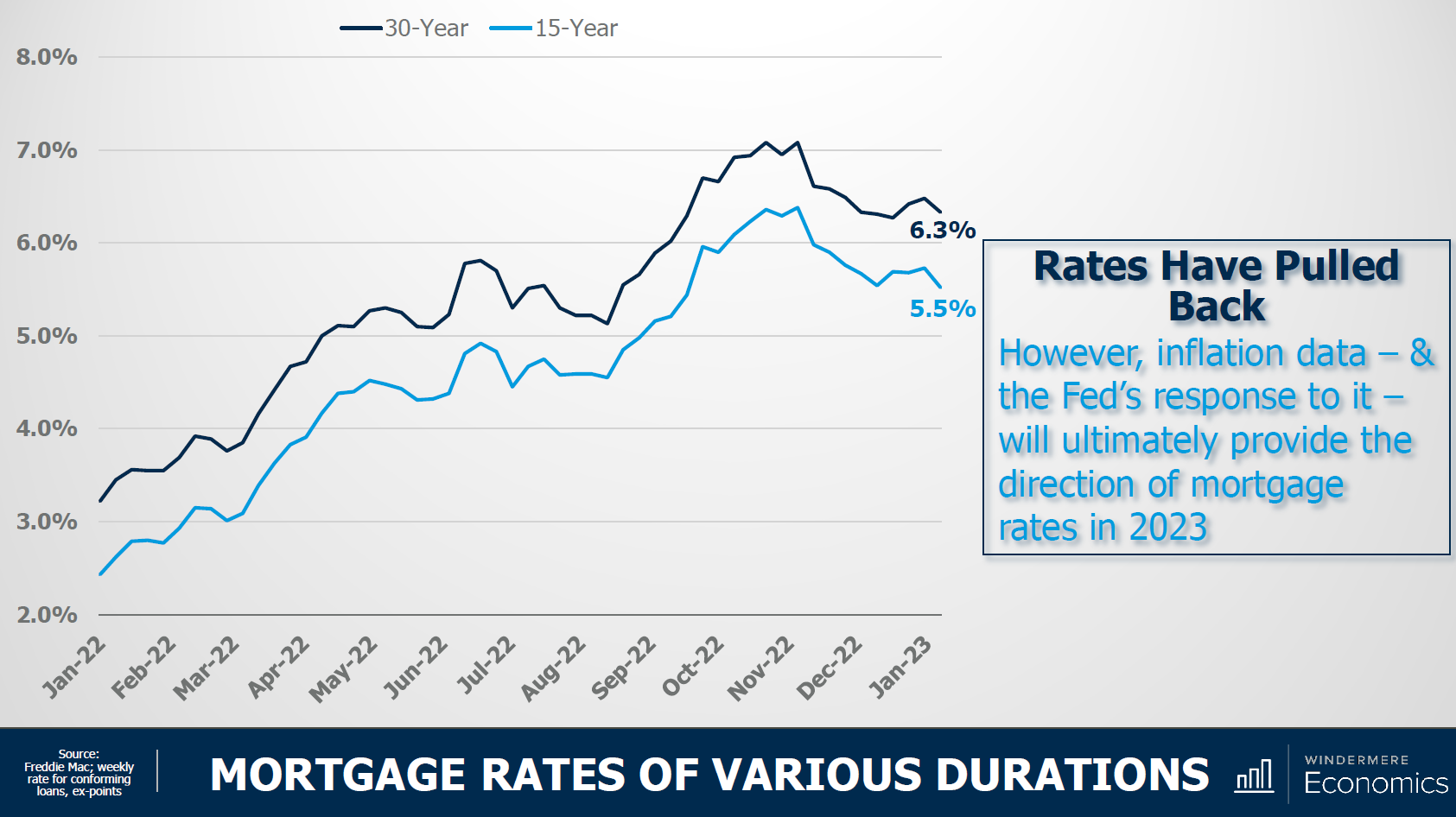

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

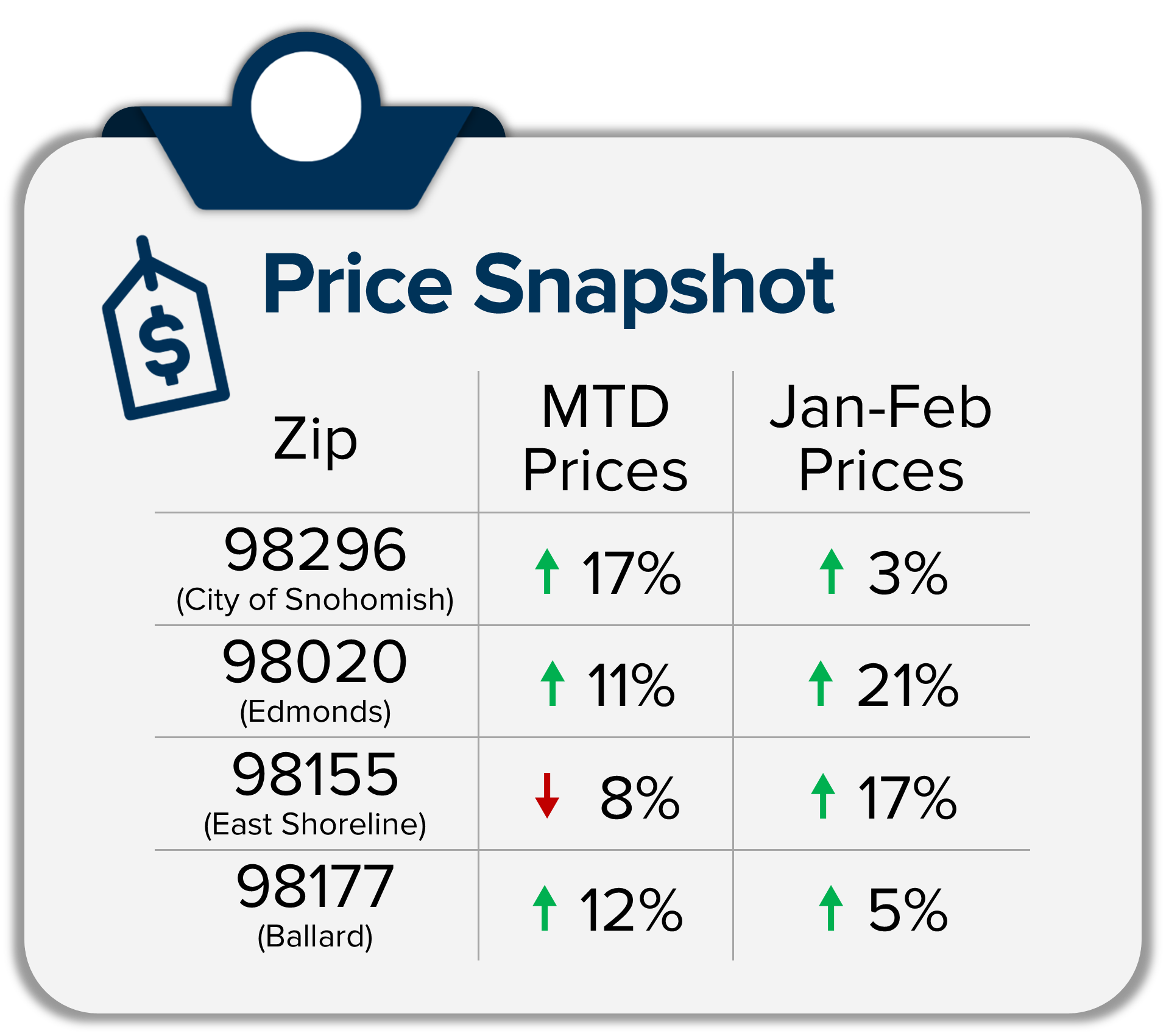

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

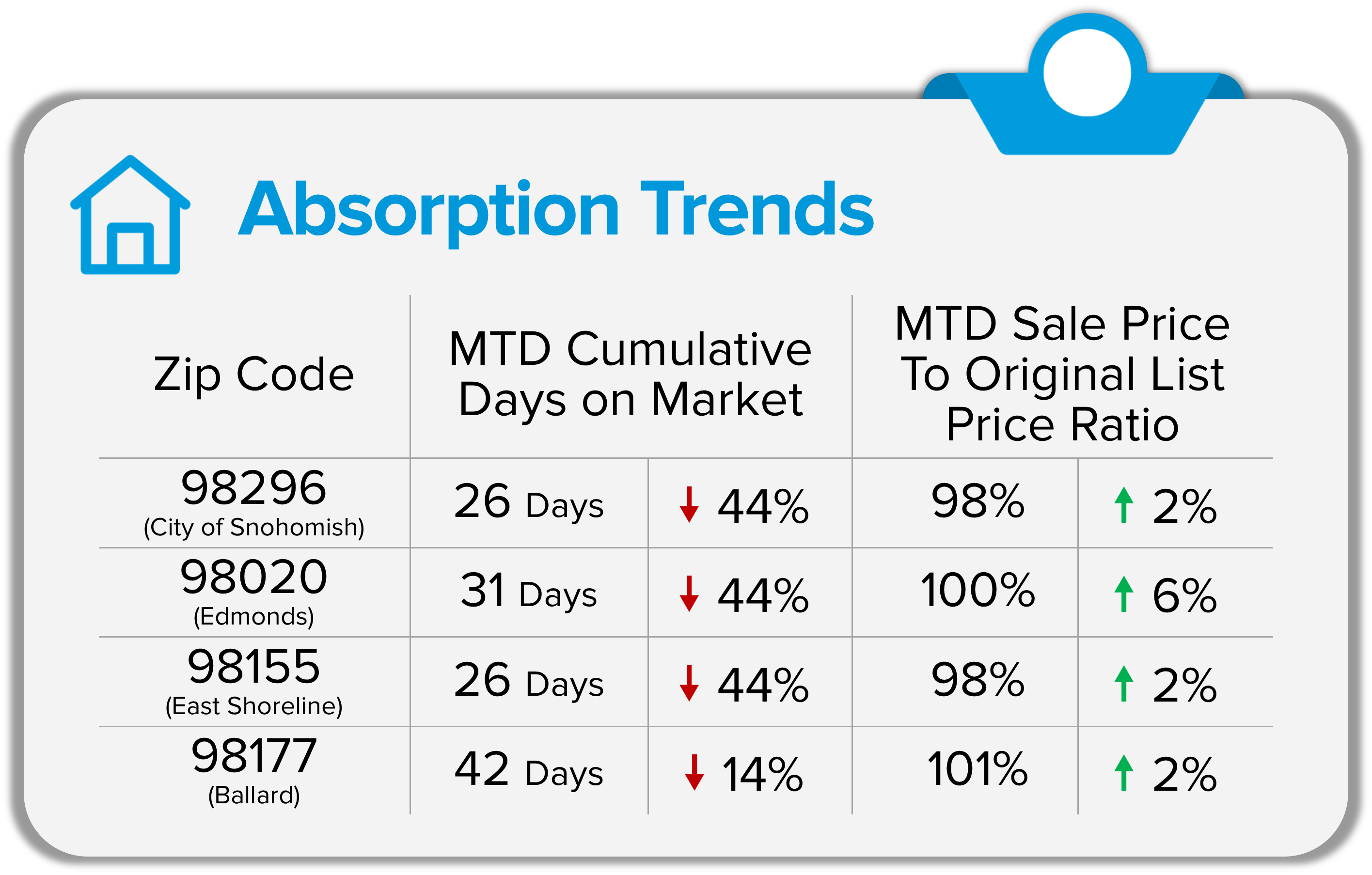

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed.

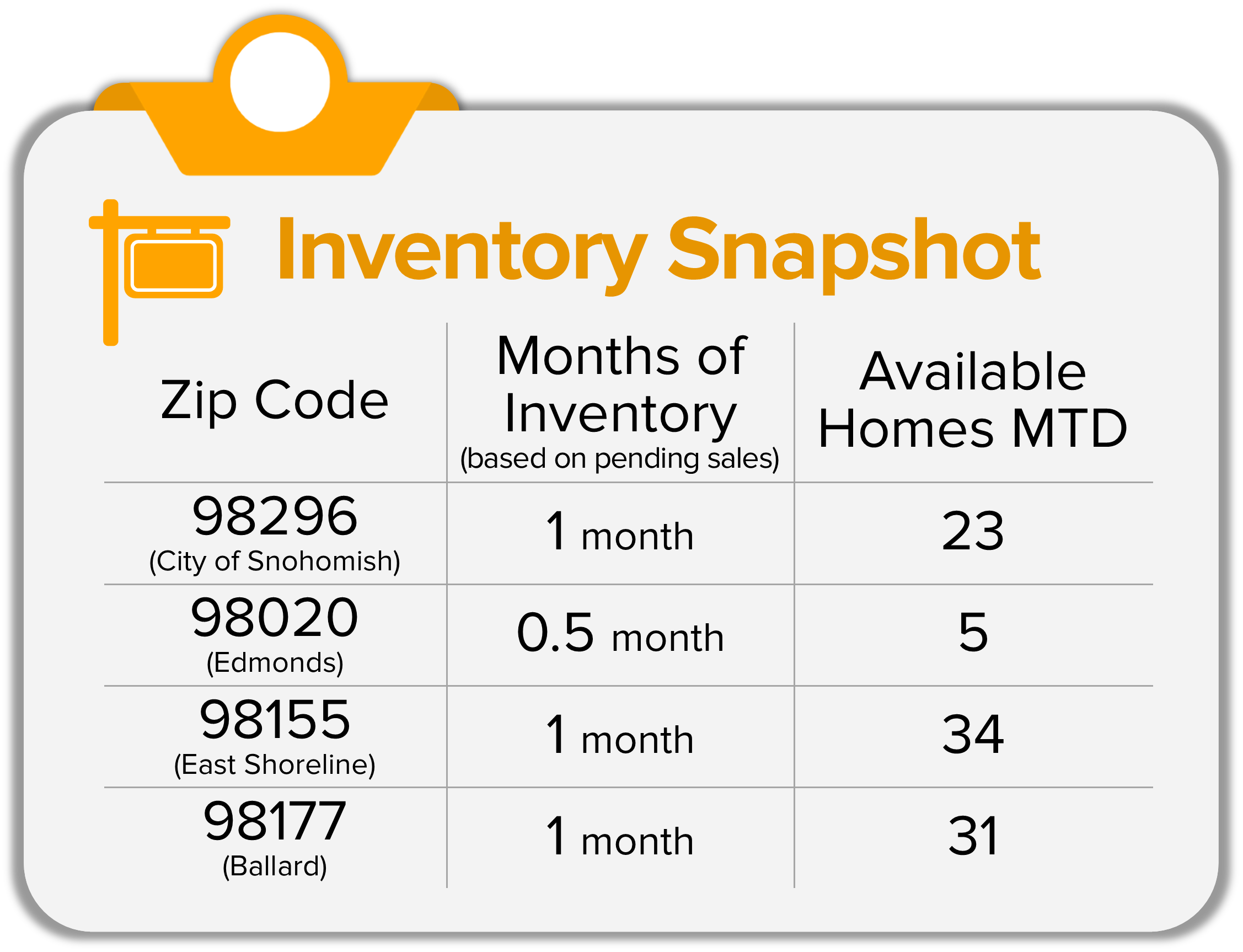

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed. Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties.

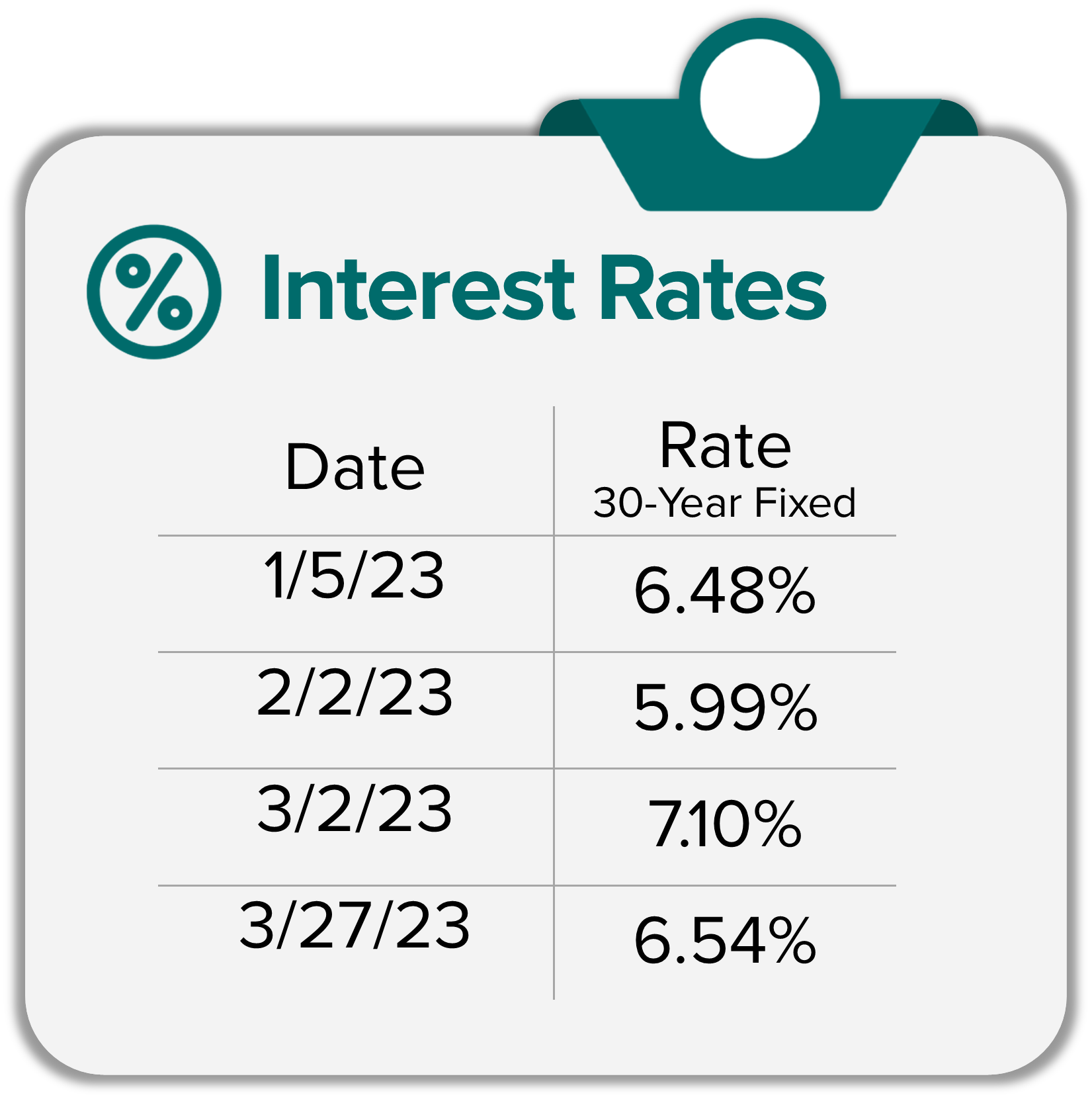

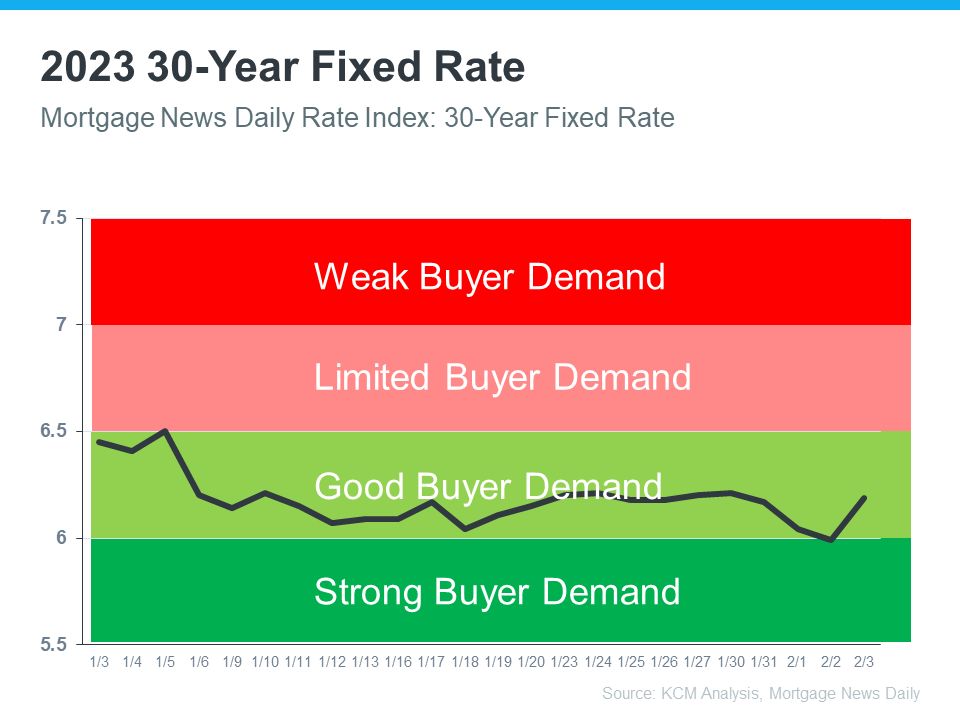

Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties. At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from

At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from  During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

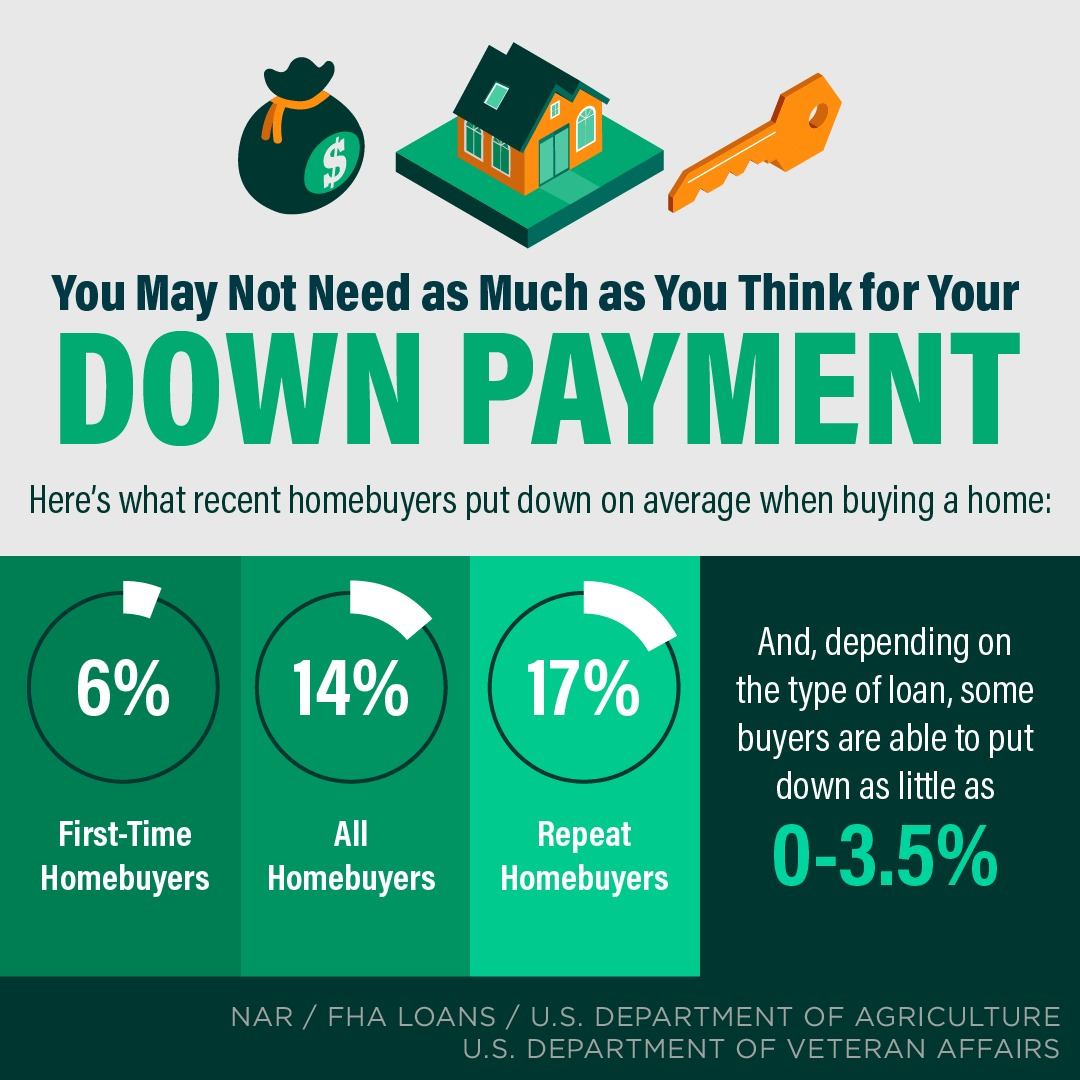

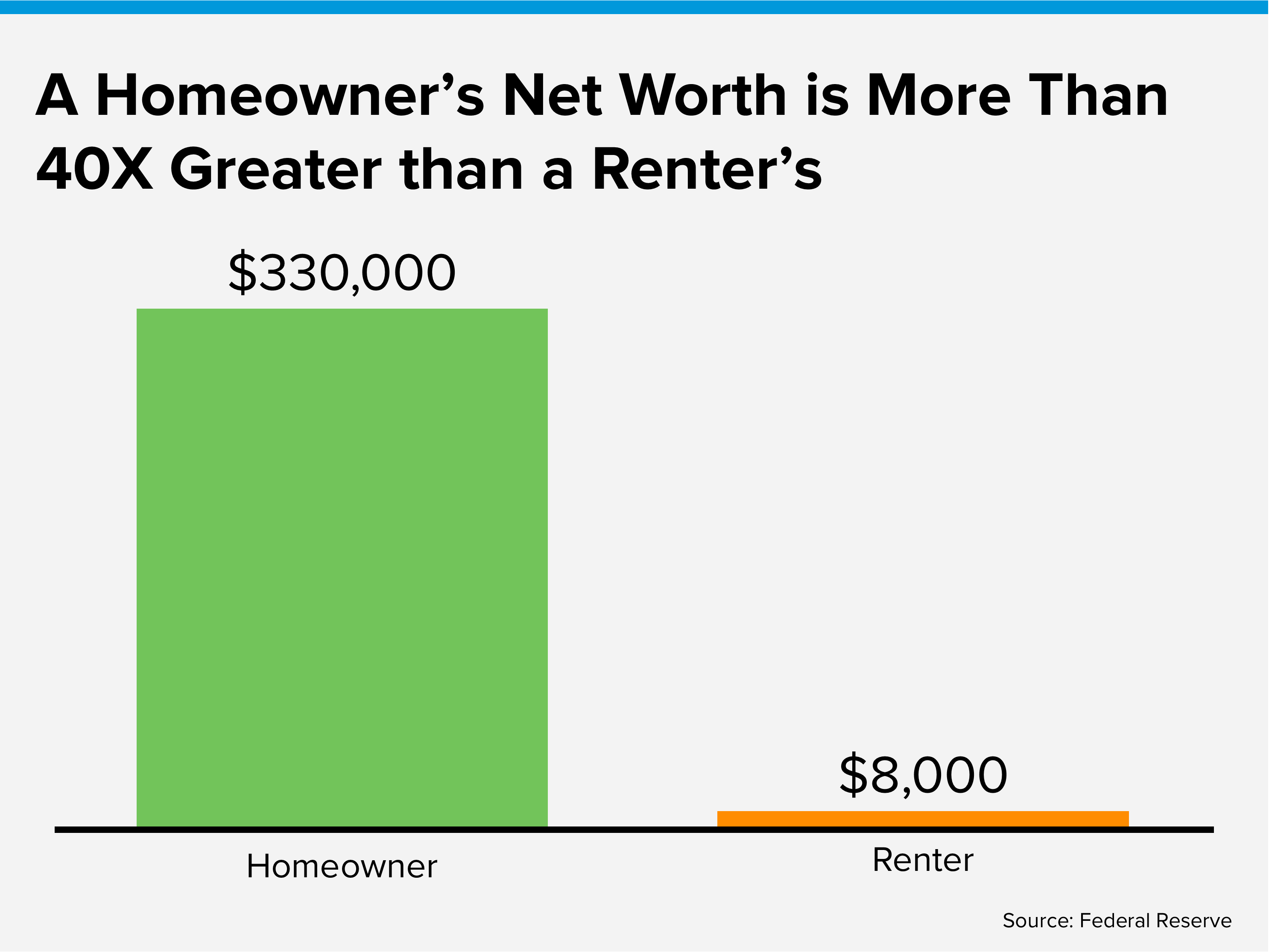

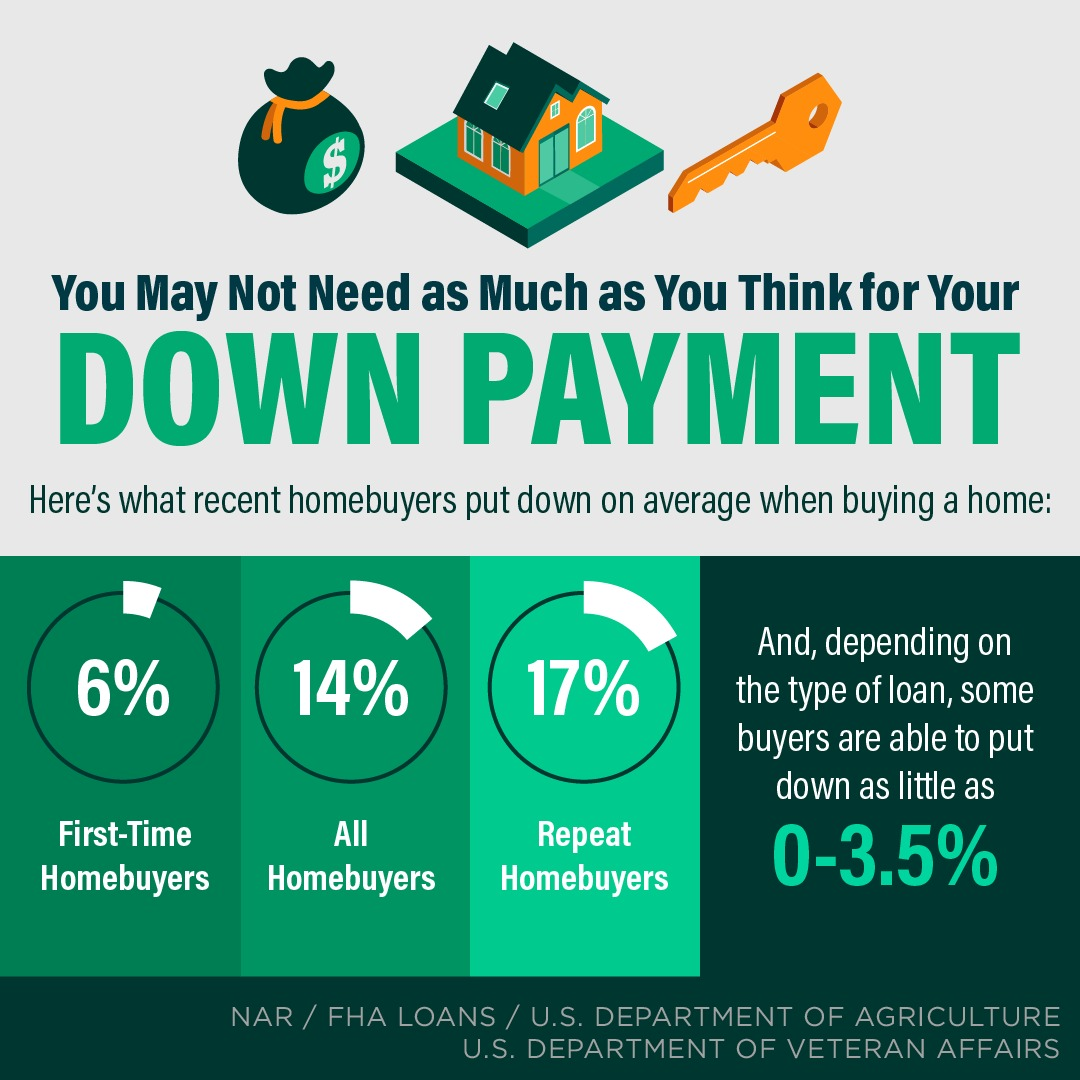

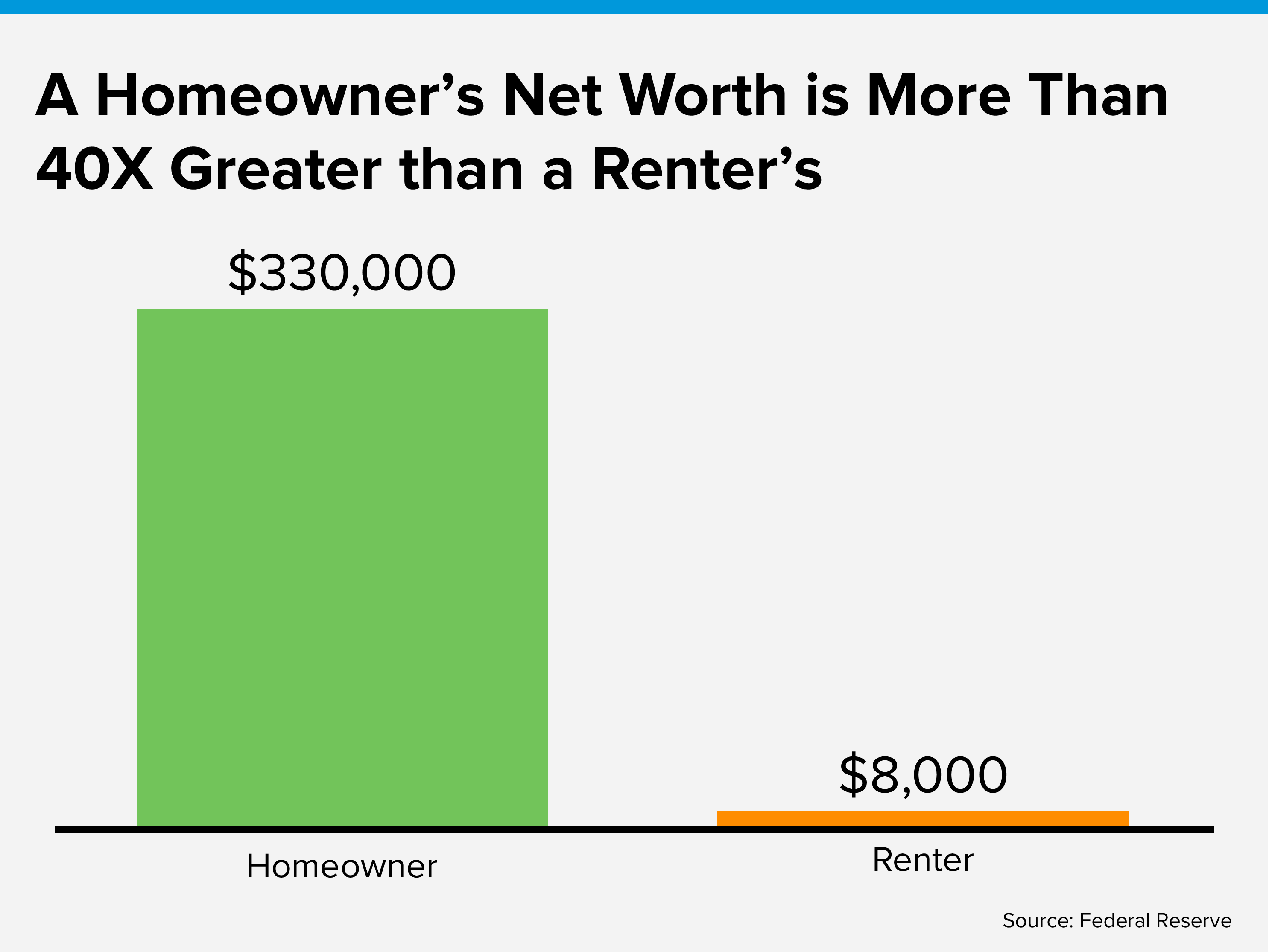

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down. Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement.

Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement. You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down.

The financial benefits of owning real estate significantly outweigh the option of renting. Renting is certainly a must for some, and is what one may have to do while they build up to becoming a homeowner. Becoming a homeowner requires solid employment, good credit, and some type of down payment. Savings can all be built over time and if achieved can provide incredible long-term financial growth by becoming a down payment on a home. In fact, many people think you need a 20% down payment in order to purchase a home and that is just not the case. There are various loan programs available requiring much less than 20% down. Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement.

Owning real estate provides tax benefits. Depending on the state you live in, you can write off your real estate taxes and mortgage interest. This can offset your tax burden and save you significant money every year. There are also capital gains tax exemptions on your primary residence that you have lived in for at least two years of the last 5 years (make sure to consult your tax expert on the details). You can have tax-free gains of up to $250,000 for a single person and up to $500,000 for a married couple. This is a wonderful opportunity to move your wealth towards your future when planning for big lifestyle improvements such as retirement. You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

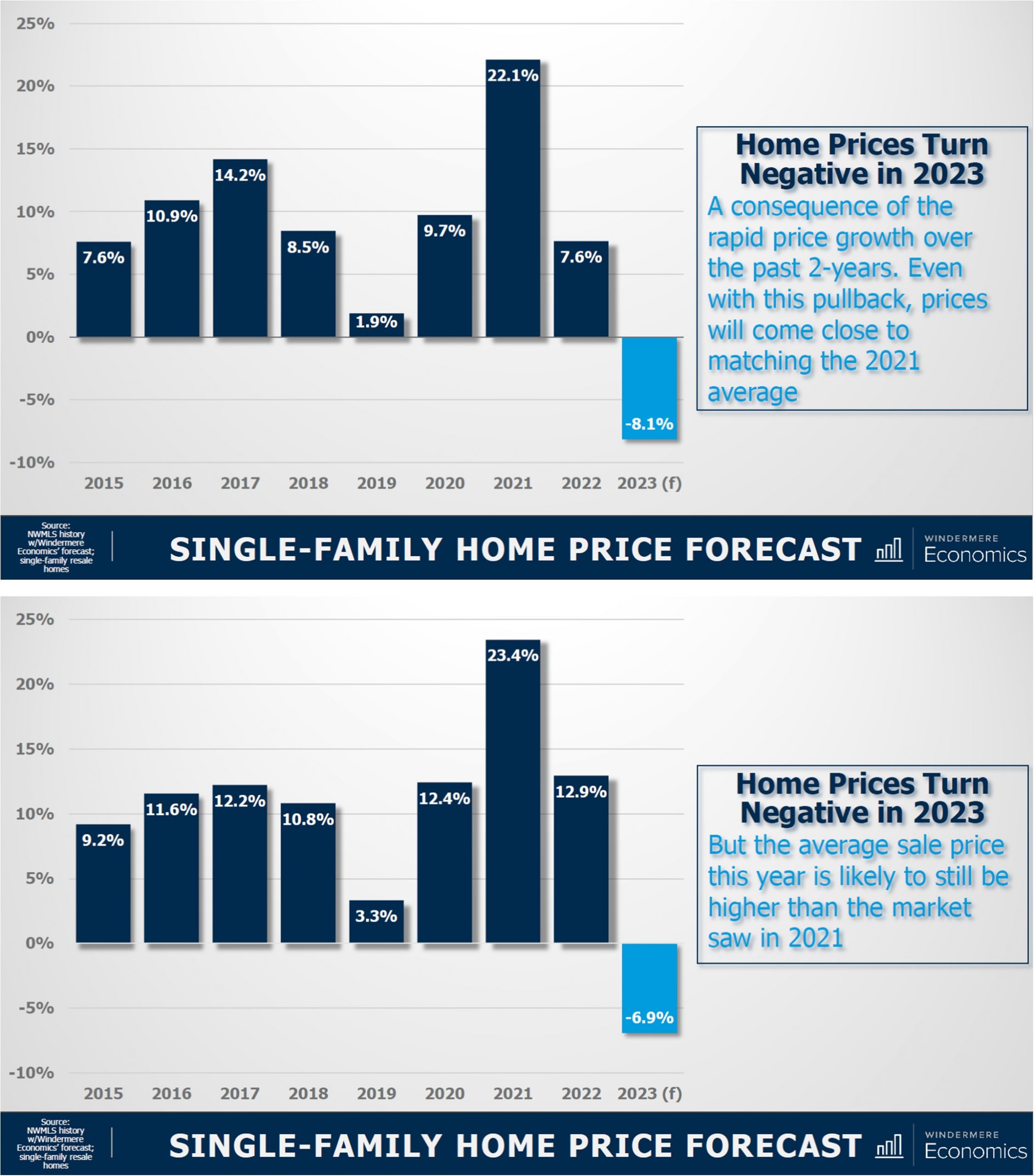

A market correction is defined by prices reverting by 10% or more. In January 2022 the median price in Snohomish County started at $700,000 then peaked at $830,000 in April, and ended the year at $689,000 (-17%). In King County, the median price started at $794,000 then peaked at $1,000,000 in May, and ended the year at $820,000 (-18%). Bear in mind that the December 2022 median price was also up 17% over the January 2021 median price in Snohomish County and up 12% in King County. This illustrates that the correction was only off the peak of spring 2022 not off of the strong equity that was built prior to that intense run-up.

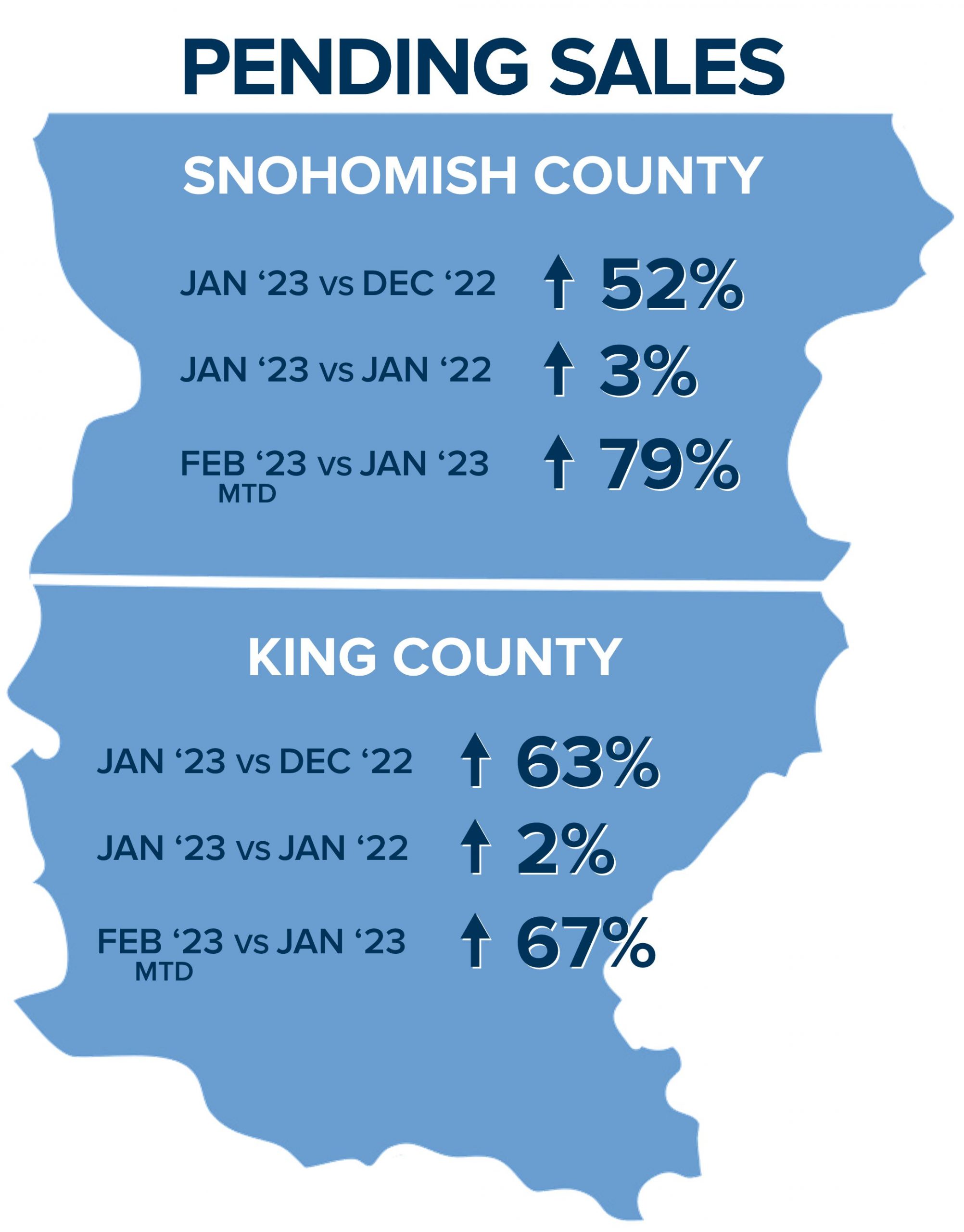

A market correction is defined by prices reverting by 10% or more. In January 2022 the median price in Snohomish County started at $700,000 then peaked at $830,000 in April, and ended the year at $689,000 (-17%). In King County, the median price started at $794,000 then peaked at $1,000,000 in May, and ended the year at $820,000 (-18%). Bear in mind that the December 2022 median price was also up 17% over the January 2021 median price in Snohomish County and up 12% in King County. This illustrates that the correction was only off the peak of spring 2022 not off of the strong equity that was built prior to that intense run-up. The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Snohomish County in January 2023 were up 52% over December 2022 and were up 3% over January 2022. Even more so an indicator: pending sales are up 80% month-to-date (MTD) in February over January 2023! In King County, pending sales in January 2023 were up 63% over December 2022 and were up 2% over January 2022, and up 61% MTD over January 2023.

The well-defined price correction and interest rates lowering have brought many buyers back to the market. In fact, pending sales in Snohomish County in January 2023 were up 52% over December 2022 and were up 3% over January 2022. Even more so an indicator: pending sales are up 80% month-to-date (MTD) in February over January 2023! In King County, pending sales in January 2023 were up 63% over December 2022 and were up 2% over January 2022, and up 61% MTD over January 2023. Real estate moves are driven by life changes. It was completely understandable that many buyers took a pause as the market corrected. Now that the market is showing signs of stabilizing these life changes are pushing buyers to find the home that better fits their lifestyle. Sellers need to keep in mind that their homes need to be priced right and show up to the market well-appointed and properly prepared to get the best results.

Real estate moves are driven by life changes. It was completely understandable that many buyers took a pause as the market corrected. Now that the market is showing signs of stabilizing these life changes are pushing buyers to find the home that better fits their lifestyle. Sellers need to keep in mind that their homes need to be priced right and show up to the market well-appointed and properly prepared to get the best results.

Last week, my office had the pleasure of hosting

Last week, my office had the pleasure of hosting  The trends across the nation are consistent, but as your local expert, along with the national forecast I am committed to reporting hyper-local facts, figures, and trends to help you understand what is happening and what will happen right in our own backyard. Our local housing market was not immune to the effects of rising interest rates. Our prices peaked in the spring and as rates climbed over 6%, prices took a tumble from the spring highs inflated by cheap money. However, prices are still higher than they were in 2021 which was a recording-breaking year of price growth.

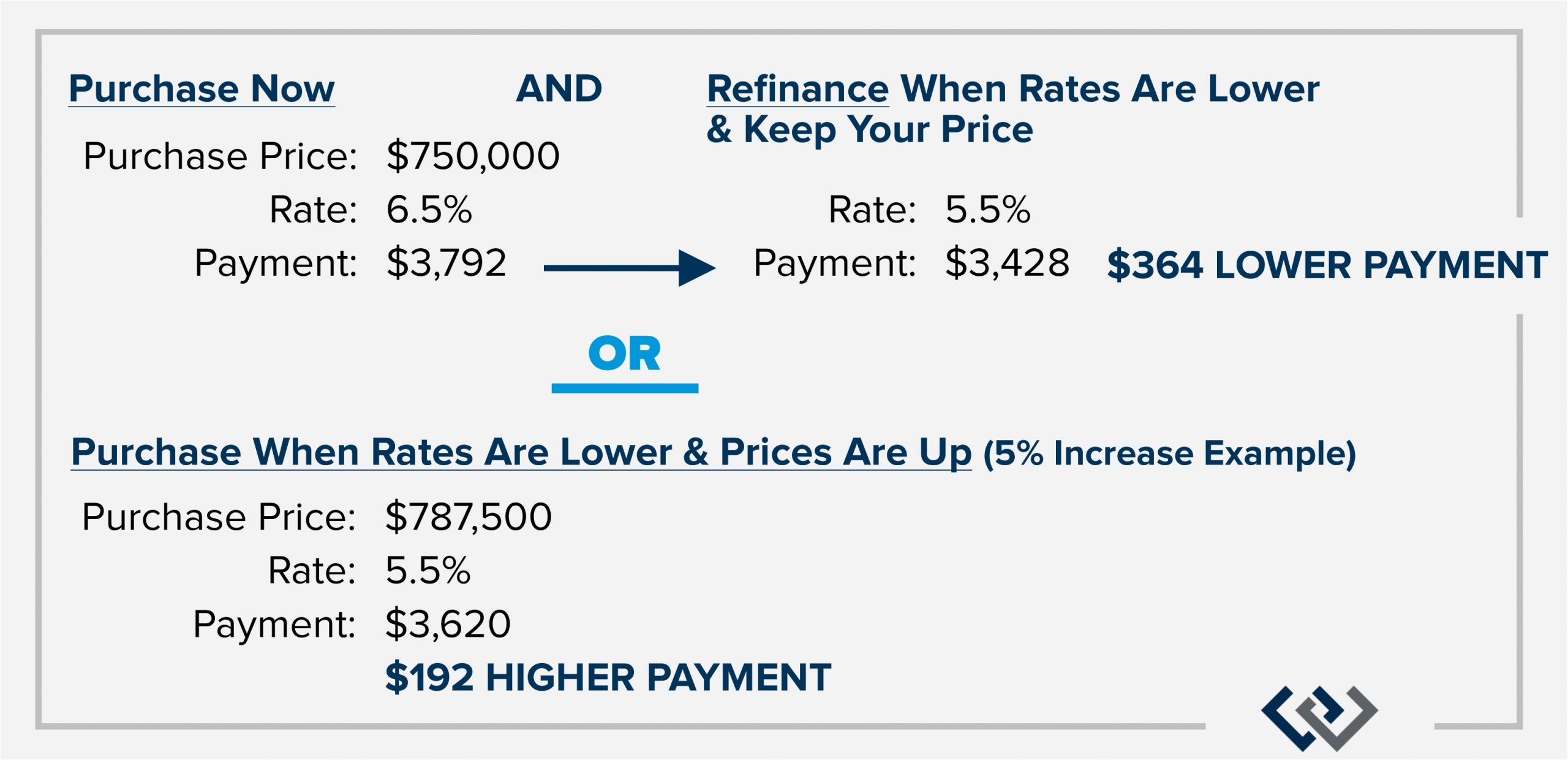

The trends across the nation are consistent, but as your local expert, along with the national forecast I am committed to reporting hyper-local facts, figures, and trends to help you understand what is happening and what will happen right in our own backyard. Our local housing market was not immune to the effects of rising interest rates. Our prices peaked in the spring and as rates climbed over 6%, prices took a tumble from the spring highs inflated by cheap money. However, prices are still higher than they were in 2021 which was a recording-breaking year of price growth. It seems that buyer demand is improving and activity is becoming more plentiful. Buyers should take note and be ready to transact if they are poised to make a move. It is a delicate dance between prices and interest rates. Buyers must understand that they can’t change their sale price once they’ve bought, but they can always refinance and change their rate. I have even heard of lenders guaranteeing a future refinance when the rate hits a certain point. Real estate is a long-term hold investment and also where you live. If where you are at doesn’t currently meet your needs, consider a move if you plan to stay there for 5+ years.

It seems that buyer demand is improving and activity is becoming more plentiful. Buyers should take note and be ready to transact if they are poised to make a move. It is a delicate dance between prices and interest rates. Buyers must understand that they can’t change their sale price once they’ve bought, but they can always refinance and change their rate. I have even heard of lenders guaranteeing a future refinance when the rate hits a certain point. Real estate is a long-term hold investment and also where you live. If where you are at doesn’t currently meet your needs, consider a move if you plan to stay there for 5+ years. Real estate is an investment and a lifestyle decision. I am committed to following experts like Matthew and others. I also study the local market trends daily. Markets change quickly and the changes are often reported far after the actual shift. I have understood these shifts due to my daily connection to the market. I take great pride in helping empower my clients to make well-informed decisions about where they live and the financial impact it has on their lives. I love what I do because it is centered in helping people with one of the biggest decisions they will make in their life. If you or someone you know are curious about how the trends relate to your goals, please reach out. I’d be honored to help educate you and help guide and strategize your next move. Here’s to a happy and healthy 2023!

Real estate is an investment and a lifestyle decision. I am committed to following experts like Matthew and others. I also study the local market trends daily. Markets change quickly and the changes are often reported far after the actual shift. I have understood these shifts due to my daily connection to the market. I take great pride in helping empower my clients to make well-informed decisions about where they live and the financial impact it has on their lives. I love what I do because it is centered in helping people with one of the biggest decisions they will make in their life. If you or someone you know are curious about how the trends relate to your goals, please reach out. I’d be honored to help educate you and help guide and strategize your next move. Here’s to a happy and healthy 2023!

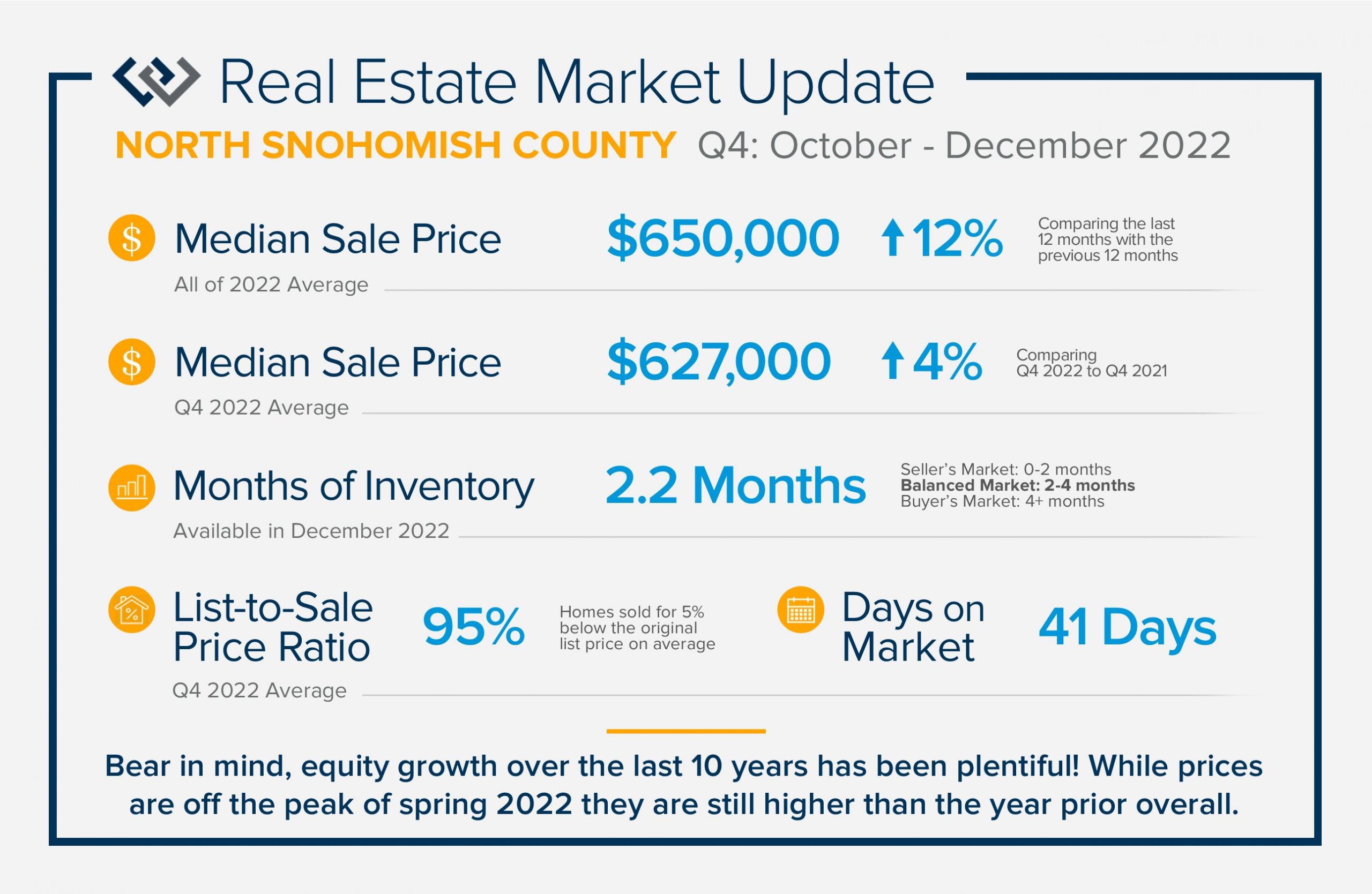

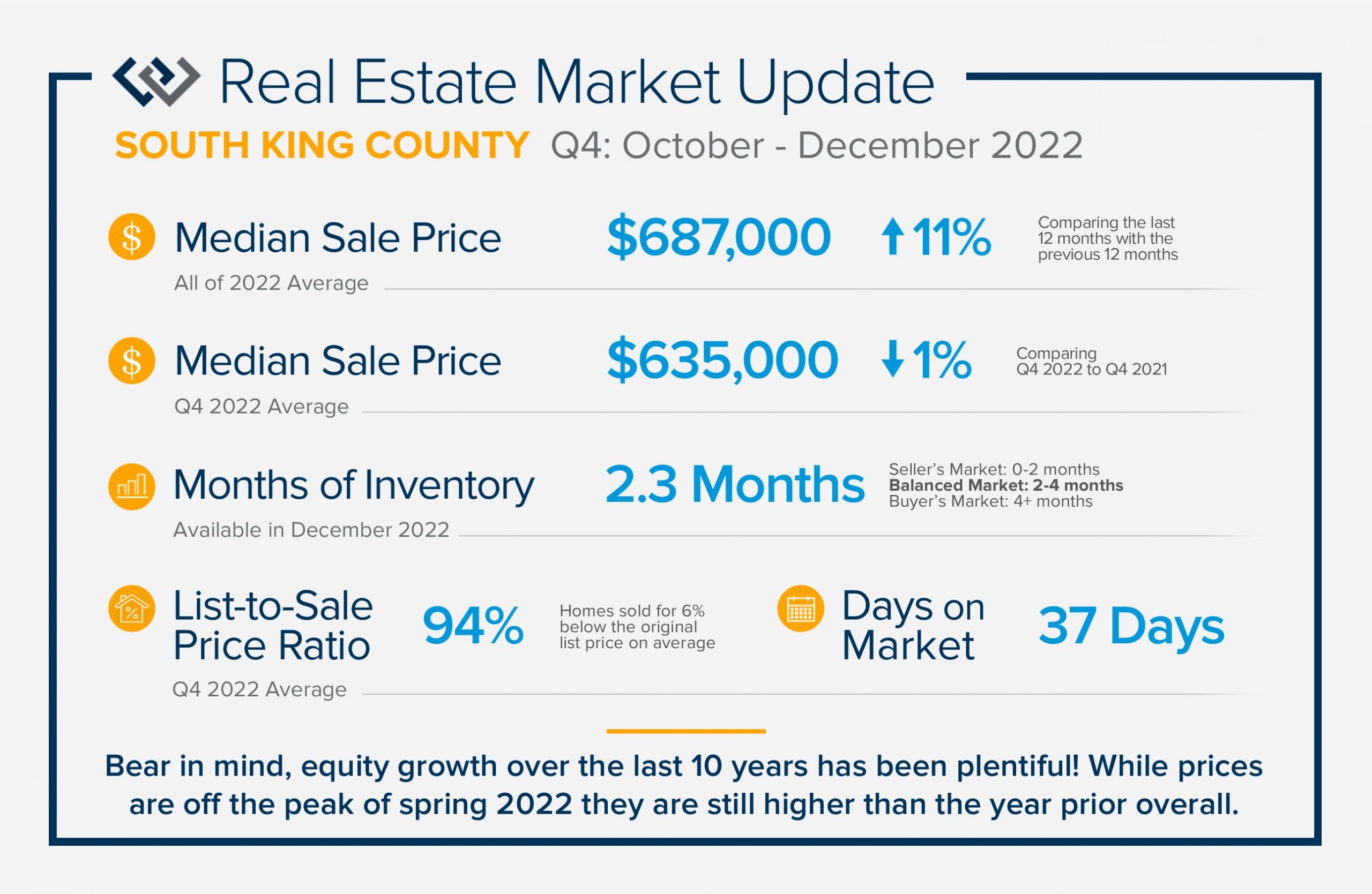

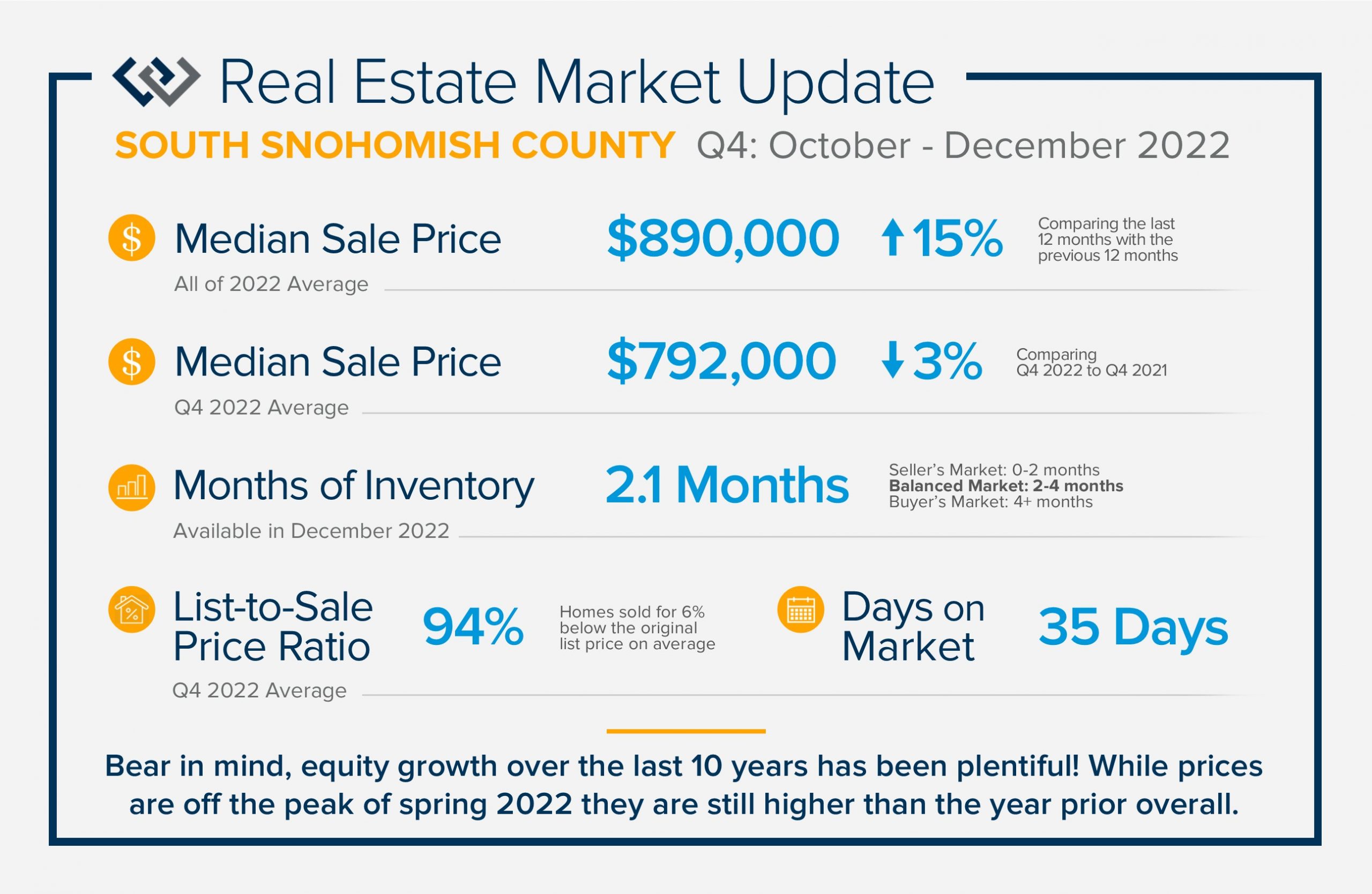

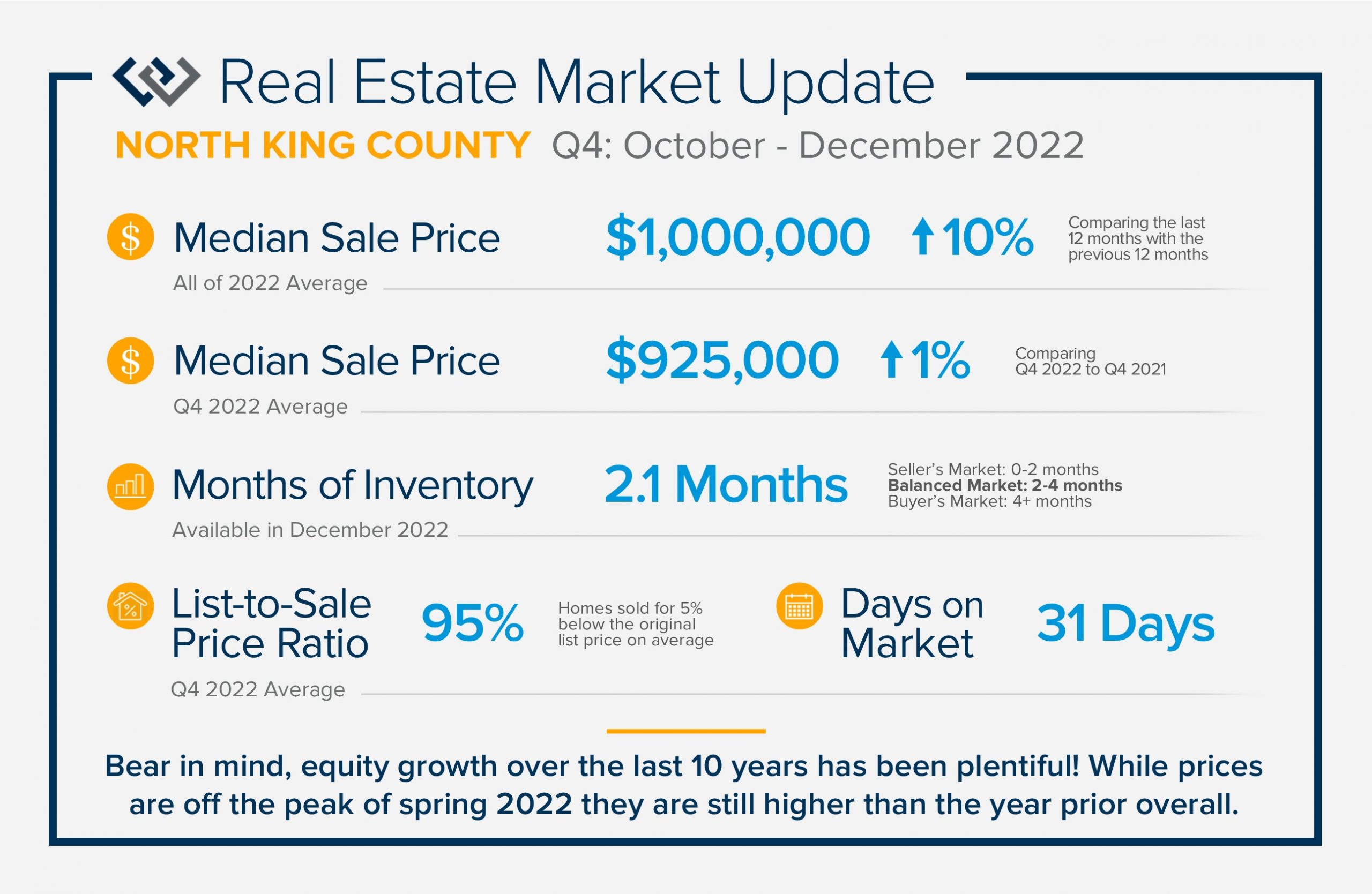

2022 was a transitional year for the real estate market that started off incredibly seller-centric and ended in balance. We started 2022 with interest rates hovering in the low 3%, peaked at 7% in late fall, and ended the year hovering in the mid 6%. This significant jump created a correction in home prices as the cost to finance a home affected affordability. Bear in mind, equity growth over the last 10 years has been plentiful! While prices are off the peak of spring 2022, they are still higher than the year prior overall. 2022 became a more traditional market with interest rates in line with historical averages, more available inventory, and the return of contract contingencies and concessions for buyers. This balance has increased days on market, highlighted the importance of accurate pricing, and made the best-prepared homes shine.

2022 was a transitional year for the real estate market that started off incredibly seller-centric and ended in balance. We started 2022 with interest rates hovering in the low 3%, peaked at 7% in late fall, and ended the year hovering in the mid 6%. This significant jump created a correction in home prices as the cost to finance a home affected affordability. Bear in mind, equity growth over the last 10 years has been plentiful! While prices are off the peak of spring 2022, they are still higher than the year prior overall. 2022 became a more traditional market with interest rates in line with historical averages, more available inventory, and the return of contract contingencies and concessions for buyers. This balance has increased days on market, highlighted the importance of accurate pricing, and made the best-prepared homes shine.